Spend enough years in finance and one contrast starts to jump out. The treasury group benchmarks itself against a national survey and knows precisely where it stands. FP&A can build three scenarios for next quarter before lunch. Then someone asks accounts receivable why a particular account is sixty days out, and the honest answer is that Linda knows, the way she has always known, because no one ever handed her team the instruments the rest of finance takes for granted.

Every corner of finance has been turned into a measured discipline over the past two decades. Accounts receivable, the function that decides whether the revenue we book ever becomes cash we can spend, is the one we still ask to run on memory, relationships, and the handful of people who carry the accounts in their heads. That was a manageable blind spot when money was cheap, and it has become an expensive one now that money is not.

The function we never learned to measure

Walk into most finance organizations, and you will find FP&A, treasury, procurement, and tax all operating with defined metrics, targets, and benchmarks. AR tends to operate with one number, DSO, and a general feel for whether collections are running ahead or behind. We treat days sales outstanding as though it captures the health of the entire function, the way you might try to describe a person's health using nothing but their weight. It tells you something real, and it hides almost everything that matters.

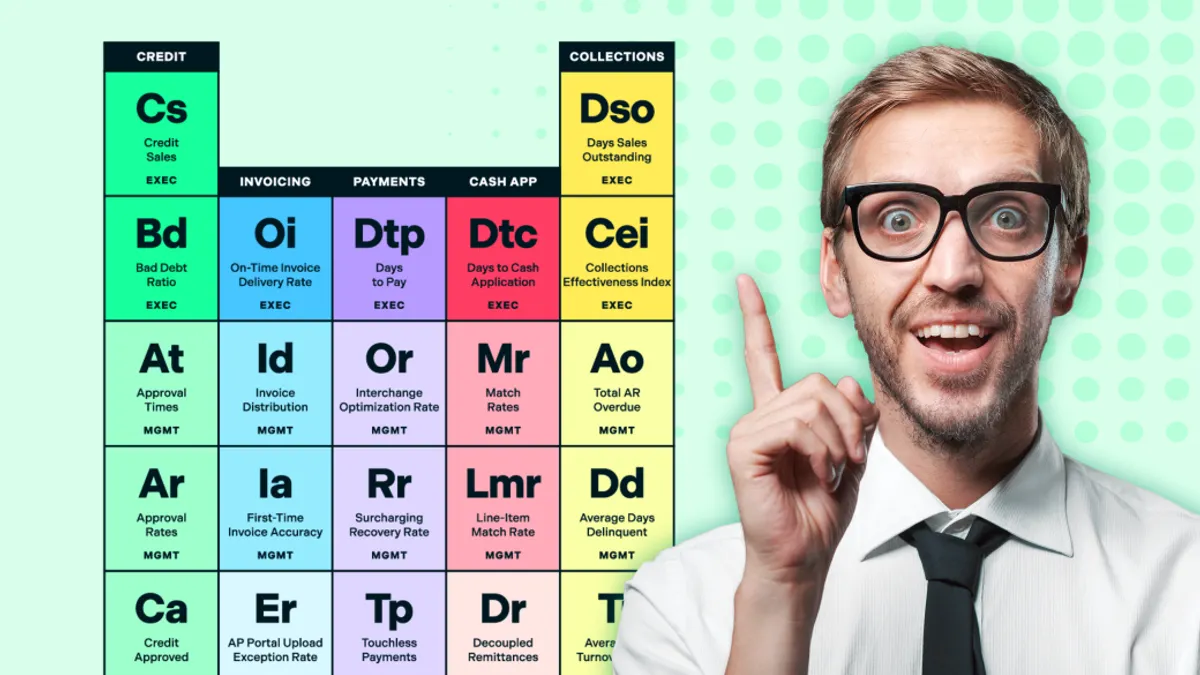

More than two dozen instruments, and most of us reach for one

When my team mapped out everything we could actually measure inside receivables, we landed on more than twenty-five distinct metrics, each one describing something specific about credit quality, collection efficiency, dispute behavior, or how cleanly cash gets applied once it lands. Collective effectiveness, bad debt ratio, average days delinquent, right-party contact rates, cash application match rates, and roughly twenty more. Each behaves like an element with its own properties, and what matters is how they combine. A clean DSO sitting beside a climbing dispute rate and a falling match rate describes a book whose real condition you would never guess from the single number most boards see.

We eventually arranged all of them out the way a chemistry class lays out the elements, grouped by what they govern and tagged for who needs to watch them, because a credit metric matters to a CFO in a very different way than it matters to the analyst chasing a single invoice. Putting the whole set in front of us made the gap obvious. Most finance teams are still managing a function with two dozen working parts by watching a single dial.

What expensive money exposed about receivables

For years, running receivables on feel was survivable, because a slow collection cost very little. When capital is close to free, a receivable that lands a few weeks late is an annoyance. When capital is expensive, that same dollar carries a financing cost for every day it sits unpaid, and those days compound across the entire ledger. In our most recent Economic Headwinds survey of finance leaders, 67% reported that their customers are paying slower than they were six months earlier, and one in five described the slowdown as significant. When that many customers stretch their timing at once, the function that manages it stops being back office and becomes a lever on working capital.

The rest of finance already treats this kind of rigor as table stakes. The Association for Financial Professionals runs a treasury benchmarking survey precisely because treasurers expect to know how they stack up, and in its most recent edition roughly 73% of practitioners ranked cash management and forecasting as their top priority. AR sits directly upstream of both, and it remains the one function we rarely hold to the same standard.

What it looks like to run AR like a science

The change begins with a decision rather than a purchase. It means treating receivables as a function that deserves to be measured as carefully as everything around it. The teams I respect most have stopped grading it against last quarter and started setting real targets for each of these metrics, the way you would set tolerances in a lab. They read the combination rather than the single dial, and they can tell a collections problem from a credit problem from an invoicing problem, because they finally measure all three as separate things instead of folding them into one number.

I have watched what this does to a board conversation. Reporting that DSO moved from forty-two to forty-five days earns a shrug and a vague promise to lean harder on collections. Reporting that the entire move came from one customer segment whose dispute rate doubled while the rest of the book stayed clean turns a soft worry into an actual decision. The underlying data is identical in both versions, and the only thing that changed is whether the function was instrumented well enough to explain itself.

Chemistry replaced alchemy the moment people stopped guessing which substances would react and started measuring why. Corporate finance has made that move nearly everywhere, and receivables is the last function we still ask to operate on feel. The Linda we keep hoping never leaves has been doing the work of an instrument panel from memory. Give her team the tools the rest of finance takes for granted, write down what healthy cash flow is actually made of, element by element, and the whole function can finally be managed to it. In an environment where every late dollar costs more than it did a year ago, this is no longer back-office hygiene. It has become a genuine source of strategic advantage for the CFO.