Many companies aren’t very smart about managing their spending, and a primary contributor to the deficiency is inadequate budgeting practices, according to research and advisory firm CEB.

More specifically, companies that use only one or two budgeting models across all business units and functions would likely make better spending decisions if they used three or all four of the most common budgeting models, a new CEB study suggests.

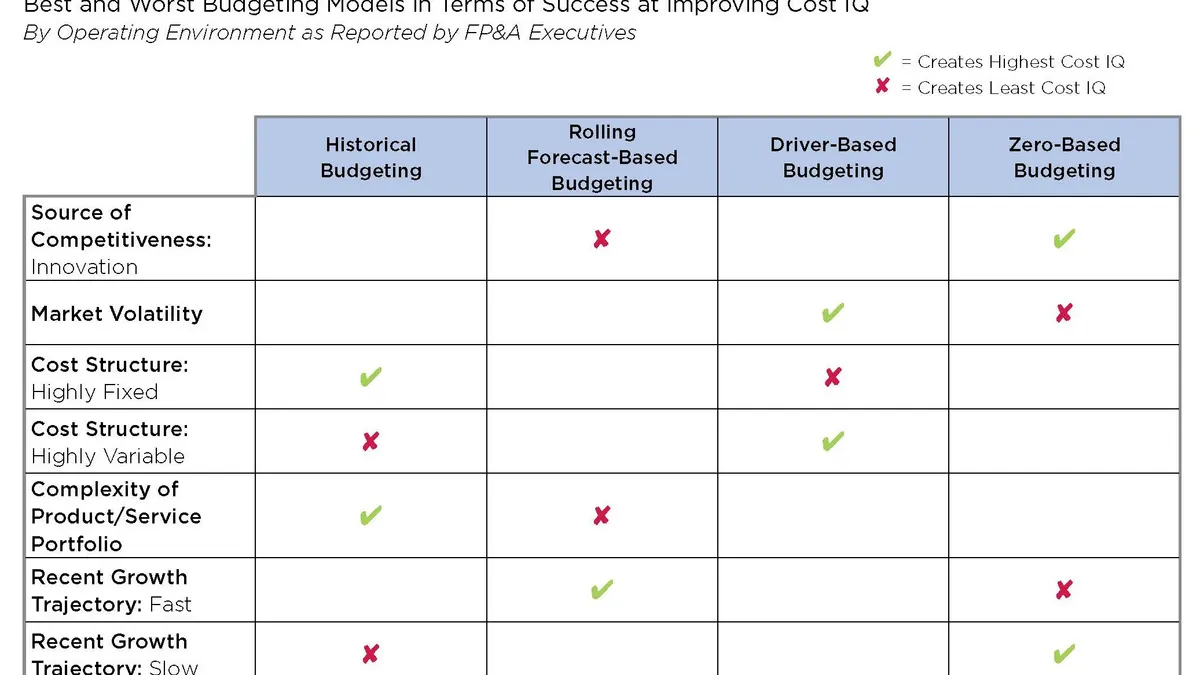

Those four models are:

- Historical budgeting, or a mix of top-down and bottom-up budgeting based on historical data, with adjustments made for factors such as expected growth and market expectations.

- Driver-based budgeting, a less-detailed approach that identifies the organization’s key business drivers and mathematically models how they will impact resourcing and, hence, expenses in future period.

- Rolling-forecast-based budgeting, where a forecast from the previous year is used to set the current year’s budget one to two quarters in advance.

- Zero-based budgeting, in which any expense in a particular cost center, department, or business unit needs to be justified for every new period.

The most efficient companies align the model used with the environment and needs of each particular business and function, CEB says. (See the sidebar and charts at the end of this article.)

Bottom-Line Impact

It’s clear that much is at stake in the budgeting choices a company makes. CEB asked 79 financial planning and analysis (FP&A) professionals, “If perfect budgeting leads to 100% achievement of your revenue and profit growth potential, how much of that growth are you sacrificing due to your current budgeting approach?”

The participants collectively estimated that their companies sacrificed 17% of both potential revenue growth and potential profit growth because of imperfect budgeting practices.

A key reason for that slippage, according to CEB, is that traditional budgeting practice, in which companies have limited variability in budgeting models used across business units and functions, does not have a positive impact on what the research firm calls “cost IQ.”

Companies with a high cost IQ have continuous visibility at the corporate level into current cost information tied to growth drivers, and not cost centers, CEB says. They also have: high confidence in current spending decisions that impact the future; explicit understanding of how costs relate to operational activities (such as how IT expenses increase with the number of employees or offices, or how travel costs vary with sales force size); and the ability to make unbiased mid-year resource allocation decisions.

Yet, only 35% of the study participants indicated that they are confident — i.e., on a 7-point scale they rated their level of confidence as a 6 or 7 — they can give corporate leaders updated expense information on business units without help from the businesses. Also, just 30% of those surveyed believed business managers would be confident making decisions based on such information.

And a mere 13% said company executives would easily understand why the updated expense information came in where it did.

“Companies’ cost IQ tends to be low,” says Johanna Robinson, finance practice leader at CEB. “It’s hard for most companies to answer questions about what their true costs are, why costs look the way they do, and what that means for future decisions. The goal is to be able to do that at any point in the year, and it’s an important goal, because it contributes directly to the bottom line.”

A big reason that cost IQ is low has to do with the mix of budgeting models used, Robinson continues. “Using three or more of the budgeting models improves cost IQ significantly,” she says.

According to CEB research, among top-quartile companies in cost IQ, where the average score is 5.63 on the 7-point scale, 55% of companies use at least three of the four budgeting models (which CEB calls “multi-model budgeting”). On the other end of the scale, among bottom-quartile companies, whose average score is 3.1, only 5% practice multi-model budgeting.

Yet only 30% of companies employ multi-model budgeting, according to CEB.

Old-Fashioned Thinking?

The research shoots holes in the main reasons that companies continue to limit the number of budgeting models they use across business units and functions.

One of those reasons is a desire to standardize budget processes. But 69% of FP&A professionals reported that multi-model budgeting processes are highly standardized (again, 6 or 7 on a 7-point scale), compared with only 39% for traditional budgeting. Companies that practice multi-model budgeting “invest in making sure that templates, timelines, and other processes are standard,” says Robinson. “It’s not the model itself that’s standardized. It’s the processes.”

Another objection to multi-model budgeting is a desire to treat businesses equally and avoid creating conflicting messages that could dilute the value of budgeting to business managers and functional heads. But 64% of survey respondents said such FP&A stakeholders perceive multi-model as valuable, while just 36% said the same for traditional budgeting.

Third, some companies think they will need to hire more consultants to implement or improve multi-model budgeting. But, according to CEB research, the proportion of companies that use consultants for those purposes is virtually the same for those that practice traditional budgeting and those that employ multi-model budgeting (35% and 33%, respectively).

Finally, some companies think diversification of models will impose a high burden on small corporate FP&A teams. In reality, however, the average size of corporate FP&A teams at companies that use traditional budgeting is 13.9, compared with 9.8 for companies that use multi-model budgeting, according to CEB.

“A lot of the work that’s done in conjunction with some of the budgeting models is actually done in the businesses,” says Robinson. “Corporate finance is more about making sure all of that flows up into corporate-level budgets.”

CEB recommends that to move to multi-model budgeting, companies should match budget models to business units and functions based on their operating attributes (see sidebar below). They also should deliberately phase in the introduction of new business models to avoid giving the organization a case of change management fatigue.

And, they should build a “budgeting 2020” framework that is based on three critical multi-model budgeting capabilities: higher analytic competence in FP&A; integration of operational and financial data; and better use of planning tools.

SIDEBAR

Mixing It Up

How does a company decide which budgeting model to use for a particular business units or functions? For business units, take a look at the two charts below (click on the charts to enlarge them). Following the charts are some thoughts about apt use of budgeting models by functions.

For functions, historical budgeting is best for those where spending is in line with traditional benchmarks; where work is largely transactional; and where work has a stable relationship to revenues.

Driver-based budgeting works for functions where the volume of work varies asymmetrically with complexity changes, like entering a new market; where there’s an established and measurable link between functional activities and cost, like sales; and where work is primarily event-driven.

Zero-based budgeting is good for functions where work is mainly project-driven. It’s also good where high service levels drive costs, such as in IT.

Functions rarely use the fourth budgeting model, rolling-forecast-based budgeting.