Technology

-

Permission granted by Dan Zhang

Q&A

Permission granted by Dan Zhang

Q&AWhy The Secret CFO calls this finance leader ‘the most AI-pilled CFO’

ClickUp CFO Dan Zhang shares why she’s proud to wear the moniker and the details of her company's extensive AI experiments.

By Adam Zaki • June 30, 2026 -

Mayuree Tipnoysanga via Getty Images

Sponsored by Salesforce

Mayuree Tipnoysanga via Getty Images

Sponsored by SalesforceBusinesses doing finance the old way risk stagnation. Agentic AI is the way forward.

Finance teams are being asked to manage more sales channels and revenue models than ever before — often with the same technology and headcount they had a decade ago. Here’s how agentic AI can help.

June 29, 2026 -

Explore the Trendline➔

Getty Images

Trendline

Explore the Trendline➔

Getty Images

TrendlineThe CFO Strategy for Artificial Intelligence

Artificial intelligence’s impact on the office of the CFO continues to evolve, and finance chiefs must be aware of the opportunities it will create for growth.

By CFO.com staff -

Getty Images

Sponsored by Billtrust

Getty Images

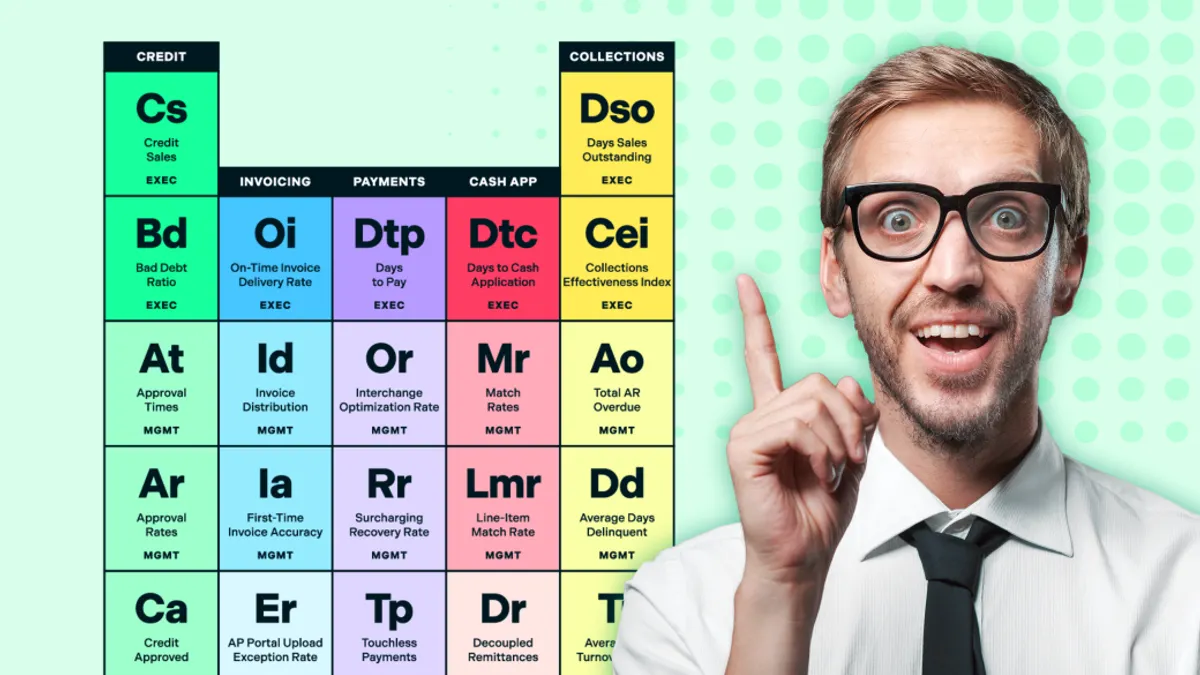

Sponsored by BilltrustAccounts receivable is the last function in finance still running on instinct

Finance evolved. AR got left behind. Here's the fix.

By David Zwick, CFO, Billtrust • June 29, 2026 -

Getty Images

Getty Images

What CFOs should do in the first 24 hours of a cyberattack

At IMA26, Walter Crawford of OakTruss Group outlined first steps to take in the wake of a major data breach.

By Adam Zaki • June 25, 2026 -

Permission granted by Paystand

Q&A

Permission granted by Paystand

Q&APaystand CFO on why banks see stablecoins as a threat

“Several years ago, anything that mentioned blockchain was instantly tied to crypto, and crypto was kryptonite,” CFO Scott Bennion tells CFO.com.

By Dan Niepow • June 25, 2026 -

Diana Gradinaru/CFO.com

Sponsored by Crowe

Diana Gradinaru/CFO.com

Sponsored by Crowe[Podcast] Transforming Tax: From Obligation to Opportunity

This podcast explores how leading CFOs are turning tax into a strategic value driver, with experts revealing how to leverage tax operations for enterprise growth and lasting competitive advantage.

By CFO.com's studioID • June 25, 2026 -

Sara D. Davis via Getty Images

Sara D. Davis via Getty Images

CFOs grow more concerned about inflation: Duke-Fed survey

Finance leaders raised cost and price forecasts while lowering expectations for economic growth in the latest quarterly survey.

By Adam Zaki • June 24, 2026 -

Getty Images

Getty Images

What CFOs would trust an agentic AI clone to do

Hasbro CFO Gina Goetter, CFO Leadership Council founder Jack McCullough and Sysdig CFO Karen Walker offer a practical look at how finance leaders are thinking about agentic AI.

By Adam Zaki • June 23, 2026 -

Getty Images

Getty Images

What’s next for corporate tax? Insights from CFO.com’s tax event

Finance leaders and tax experts shared insights on tax scams, inevitable tax increases and AI's role in tax at the “Navigating the Corporate Tax Frontier” event.

By Lauren Muskett • June 22, 2026 -

Permission granted by Karen Walker

Q&A

Permission granted by Karen Walker

Q&ASysdig CFO Karen Walker on scaling without perfection

The Sysdig finance chief reflects on a career spent scaling fast-growing companies and explains why the CEO-CFO relationship remains one of the most important in the business.

By Adam Zaki • June 18, 2026 -

Getty Images

Opinion

Getty Images

OpinionAI is eroding trust. Accounting and finance professionals can rebuild it

Finance teams are uniquely positioned to restore confidence by pairing AI tools with human judgment, stronger oversight and practical upskilling.

By Mike DePrisco • June 16, 2026 -

Permission granted by Michael Silvano Photography

Permission granted by Michael Silvano Photography

Vertex Pharmaceuticals CFO’s case for thinking like a portfolio manager

After helping scale Vertex Pharmaceuticals from $3 billion to $13 billion in revenue, CFO and COO Charles Wagner says finance leaders must build organizations for opportunities that haven’t emerged yet.

By Adam Zaki • June 16, 2026 -

Spencer Platt via Getty Images

Spencer Platt via Getty Images

SpaceX CFO Bret Johnsen joins billionaire ranks after $75B IPO: Trial Balance

The space technology company’s recent IPO reveals the scale of Johnsen’s long-held equity stake.

By Adam Zaki , Lauren Muskett • June 15, 2026 -

Getty Images

Getty Images

Most midsized companies now use AI for FP&A

A majority of C-suites have mandated that the finance function apply the technology to internal processes, according to a recent vendor survey.

By David McCann • June 15, 2026 -

stock.adobe.com/Dima Sikorski/Stocksy

Sponsored by Crowe LLPFrom exploration to scale: A road map for AI in tax

Adopting AI in tax is a journey – it’s important to start small and scale wisely. Discover how tax teams can take a phased, thoughtful approach to AI.

By Matt Paparella, Tracey Grant-Castleman • June 15, 2026 -

BlackJack3D via Getty Images

BlackJack3D via Getty Images

Why some CFOs are saying no to digital clones, for now: Peer Audit

Big Tech leaders are enthusiastic at the prospect of using AI-created versions of themselves to handle earnings calls, media interviews and more, but finance leaders are taking a more measured stance.

By Dan Niepow • June 12, 2026 -

Justin Sullivan via Getty Images

Justin Sullivan via Getty Images

OpenAI CFO Sarah Friar offers a look inside the company’s finance function

On a recent webcast, Friar discussed how the company’s roughly 200-person finance team approaches investor relations, tax compliance, pricing and economic research.

By Adam Zaki • June 11, 2026 -

Getty Images

Getty Images

Companies save cash with AI, but less than expected

The gap between projected and actual return could widen further with increasing investments in complex new tools.

By David McCann • June 11, 2026 -

Getty Images

Getty Images

What counts as value? EY says CFOs need new metrics

Markets and strategy leader Myles Corson told CFO.com that finance leaders need broader ways to measure value as AI and business transformation challenge traditional performance benchmarks.

By Adam Zaki • June 10, 2026 -

Permission granted by Michael Silvano Photography

Permission granted by Michael Silvano Photography

Wayfair CFO says pandemic hangover is building a stronger company

After years of layoffs and slowing demand, Kate Gulliver says a leaner organization with smaller teams and simpler incentives is now executing more effectively.

By Adam Zaki • June 9, 2026 -

Getty Images

Getty Images

SMBs ramp up AI tool use to manage company and employee expenses

The complexity of expense management is increasing as companies work with more vendors and increasingly adjust spending policy.

By David McCann • June 8, 2026 -

Permission granted by Christy Totin

Q&A

Permission granted by Christy Totin

Q&ANet Health CFO on shifting from apparel retail to niche SaaS

Christy Totin discusses the appeal of healthcare software financial leadership after a decade in retail finance.

By Sandra Beckwith • June 4, 2026 -

Getty Images

Getty Images

9 questions heading into the CFO Leadership Council’s 2026 Spring Conference

From controlling healthcare costs to the rise of the COFO role, this week's conference agenda reveals the most pressing challenges facing finance leaders today.

By Adam Zaki • June 2, 2026 -

Getty Images

Sponsored by Cleverbridge

Getty Images

Sponsored by CleverbridgeSoftware sprawl is becoming a margin problem for SaaS CFOs

The next phase of SaaS will reward companies that combine commercial ambition with operational discipline.

By Markus Scheuermann, CFO, Cleverbridge • June 1, 2026 -

martin-dm via Getty Images

martin-dm via Getty Images

Mid-market CFOs confront growing execution strain

During H1 2026 discussions hosted by the CFO Alliance, finance leaders describe rising pressure tied to AI implementation, healthcare inflation and operational resilience.

By Adam Zaki • May 29, 2026